A Registered Education Savings Plan (RESP) is widely acknowledged as the number one way to save for a child’s education. However, many Canadians use an RESP as the foundation and complement the plan with another investment vehicle.

Why would parents or grandparents choose an additional way to invest? Usually, it’s to accumulate more savings or gain enhanced flexibility.

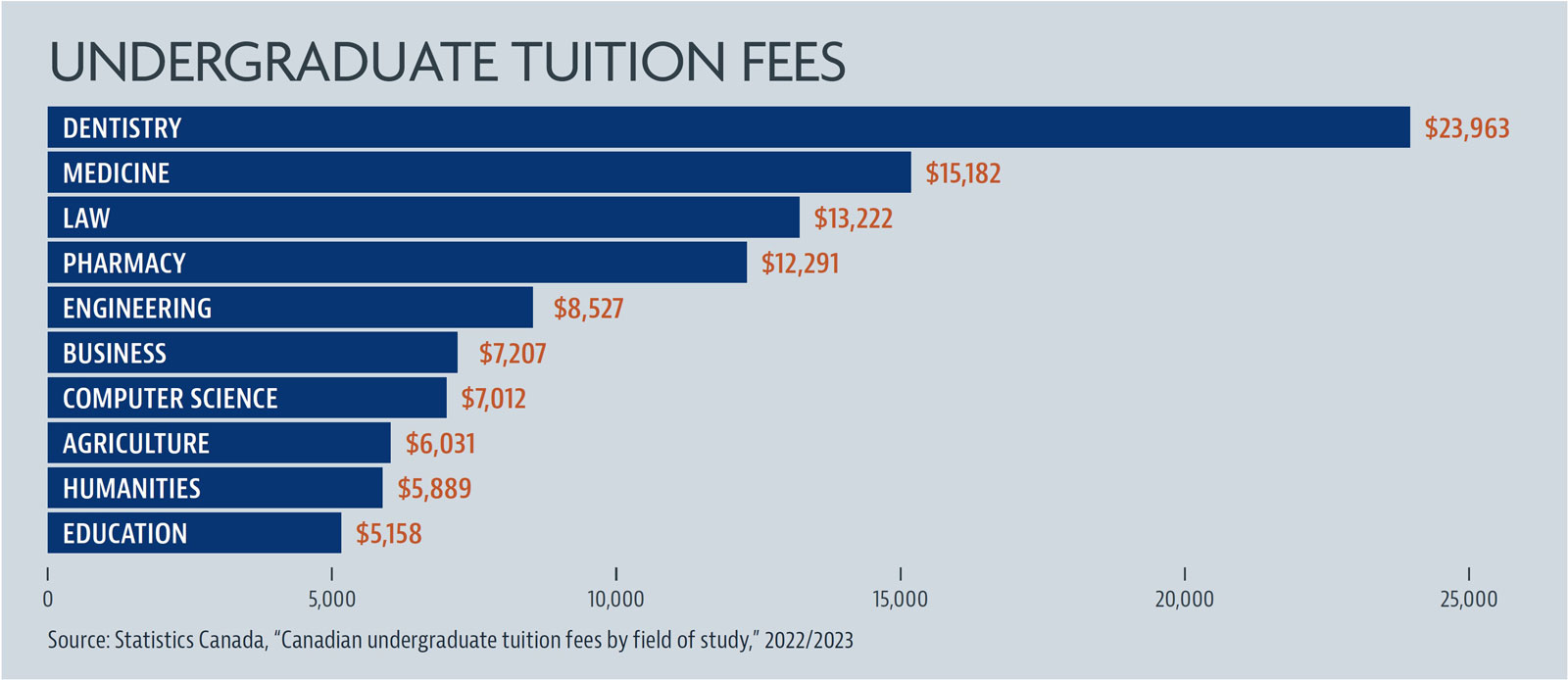

WHEN COSTS MAY ESCALATE

You could plan your education savings goal around expected costs, only to experience the unexpected. Perhaps throughout their school years a child always talked about being a teacher, but in Grade 12 they decide to become a physician—at three times the tuition. Or after a couple of years in university or college, they want to begin a different program, requiring extra years of funding. A student might complete a college program and then decide to enrol in a university program, or vice versa. Your child or grandchild might receive a bachelor’s degree and decide to pursue a graduate degree. Perhaps they want to attend a higher-tuition university in the U.S. or abroad.

If you plan for average education costs and the actual costs exceed your education savings, you may need to cover the difference with funds from somewhere else.

VEHICLES TO GET YOU THERE

Several options are available to save for post-secondary education. Here are the most common vehicles.

RESP. You can contribute up to $50,000 for each child, with no annual limit. RESPs offer tax-deferred growth, but for many investors the most compelling benefit is the Canada Education Savings Grant (CESG). The first $2,500 you contribute each year triggers a $500 deposit into your plan. That’s like getting an immediate 20% return on your investment. You can receive up to $7,200 in CESG money per child.

Tax-Free Savings Account (TFSA). With tax-free growth and withdrawals, your TFSA can be an ideal way to supplement education savings. In addition to withdrawals being tax-free, they don’t require special planning. Withdrawals from an RESP, some of which are taxable, can involve planning in two situations. One is when pay from a summer job or co-op placement places a student’s income beyond the personal exemption amount. The other is when the child doesn’t pursue post-secondary education or if unused funds remain in the plan.

In-trust account. An in-trust account, also known as an informal trust or “in-trust for” (ITF) account, is a non-registered account that a parent or grandparent can set up—quite easily—for a minor child. Typically, it’s used for investing in equities—as capital gains are taxable to the child, which usually results in little or no tax to be paid. Interest and dividend income are taxable to the contributor, unless that income is realized from contributions of Canada Child Benefit payments or an inheritance. Note that you must file a T3 return each year to report trust income. Also, be aware that the account’s assets belong to your child or grandchild upon reaching the age of majority.

In-trust accounts with investment earnings taxable to a minor are not available to Quebec residents.

Non-registered account. A simple option is to dedicate a non-registered investment account to education savings. If a parent with low income opens an account, this choice could offer investment growth with little or no tax payable.

Talk to us if you’re thinking about supplementing your RESP with another investment vehicle. We can discuss the various options and recommend one or more choices that suit your personal situation.